The Ohio Housing Needs Assessment uses a wide range of data to identify the scale and scope of Ohio's housing challenges. As part of OHFA's annual planning process, the assessment plays a critical role in providing baseline information that the Agency uses to determine its strategic priorities. The following executive summary highlights the key trends related to affordable and accessible housing throughout Ohio.

The rate of homeownership in Ohio has started to decline after a period of improvement from 2017 to 2020 when the rate reached a 10-year high of 70%. By the end of 2022, the rate had fallen to 64% – lower than the national average for the first time on record.

Home sales have steadily declined since the start of the pandemic. In 2022, there were 209,612 homes purchased in Ohio – the lowest annual number since 2015.

In 2022, the median home price in Ohio ($174,000) was higher than in any year on record other than 2021 when adjusted for inflation.

The median home price in Ohio in 2021 was 2.6 times the median household income – the largest price-to-income ratio since 2005 – making homeownership more unaffordable to many prospective homebuyers.

Mortgage holders are spending less on housing than they were a decade ago – both the median monthly costs relative to inflation ($1,293) and median share of income spent on housing (19%) are the lowest figures on record.

At the same time, the prevalence of severe mortgage burden is on the rise. In 2021, 8.4% of Ohio mortgage holders were spending at least half their income on housing – up from a record low of 7.2% in 2019 – putting them at risk of mortgage default and foreclosure.

Vacancy rates have been falling steadily since 2009. In 2021, both homeowner and rental vacancy rates hit their lowest recorded levels – 0.4% and 4.0% respectively. At the end of 2022, these rates remained relatively low – 0.9% and 6.2% respectively – indicating an extremely tight housing market.

From 2016 to 2021, there was a 38% decline in the number of vacant units available for sale or rent. In the same period, there was a 13% increase in the number of units for seasonal, recreational, or occasional use, including short-term rental properties. These changes to the available housing supply are huge obstacles for prospective homebuyers and renters on fixed incomes.

Ohio renters are spending more on rent. Adjusted for inflation, median gross rent in Ohio increased by 10% from $788 per month in 2012 to $870 per month in 2021. Rent is higher than in any year on record other than 2021 when adjusted for inflation.

The increase in income for the 80th percentile of Ohioans since 2006 has outpaced the increase in rent over that period while the income level at the 20th percentile has generally lagged since 2008. As such, Ohio renters are spending more relative to income. The median share of income spent on rent (28%) is steadily increasing after a decade of decline.

The prevalence of severe rent burden is also on the rise. In 2021, 25% of Ohio renters were spending at least half their income on housing – up from a record low of 23% in 2019 – putting them at risk of eviction and homelessness.

New residential construction has been steadily increasing since 2009; however, production is still far below pre-recession levels. In 2022, 30,936 new privately-owned housing units were constructed in Ohio, representing a 29% increase from 2017. Compared to neighboring states, Ohio had the greatest increase in private residential construction over this period.

This construction boom is primarily driven by increased production of multifamily units (71% growth) – including condominiums and market-rate rental housing. Over the same period – by comparison – single family housing construction only increased by 8%.

At the same time, there has been a net loss of affordable rental housing for the lowest income Ohioans. There are 447,717 extremely low-income (ELI) renters in Ohio, but only 177,318 rental homes are affordable and available to them – leaving a shortage of 270,399 units.

The affordability gap between supply and demand for the lowest income renters is now widening with a net loss of more than 15,000 affordable units between 2020 and 2021.

Over 1 million Ohioans (8.8%) live in a household that spends at least half its income on housing, which puts them at risk of foreclosures or evictions. This includes 325,722 people living in households that are severely mortgage-burdened and 707,820 Ohioans living in severely rent-burdened households.

Ohio's 90-day delinquency rate rose sharply in 2020 due to the COVID-19 pandemic – peaking at 3.9% in August of that year. The serious delinquency rate has since returned to pre-pandemic lows (1.5% in December 2022).

While there were more delinquencies throughout the height of the pandemic, foreclosures remained low due to the federal foreclosure moratorium, which expired on July 31, 2021. As such, Ohio's foreclosure rate reached a historic low of 0.3% in December 2021, but since then, foreclosures have been on the rise (0.5% in December 2022).

From the start of the pandemic, the threat of eviction loomed large. Thanks to both local and federal moratoria on eviction proceedings combined with emergency rental assistance, Ohio's eviction filing rate dropped from 6.6% in 2019 to 4.2% in 2020. With the expiration of these eviction moratoria in 2021, however, eviction filings have returned to near pre-pandemic levels (6.4% in 2022).

As a result of the COVID-19 pandemic, more Ohioans are working from home. In February 2020, one in five business establishments in Ohio allowed at least some of its employees to telework – accounting for 25% of the workforce. By September 2022, one in four Ohio establishments allowed working from home, which increased the share of the workforce that can telework to 36%. This includes 3% who work remotely all the time.

At the same time, many Ohioans lack the reliable internet services necessary to work from home. One in eight Ohio households (12%) lacks a broadband subscription, which limits access to reliable internet services. This is higher than the national average (11%). Reliable internet access is most lacking in Southeast Ohio where 22% of homes either have no broadband subscription or no computer.

Ohio's housing stock is relatively old. One in four housing units in Ohio (or 25%) was built before 1950 when the nation's first laws banning lead-based paint were enacted – higher than the national share (16%). Northwest Ohio has the highest share of pre-1950 homes (31%). These homes are more likely to contain chipped lead paint or lead-contaminated dust, which can be ingested by young children.

Due in part to the age of Ohio's housing stock, 62% of housing units in the state are in buildings that require entry steps – much higher than the national average (47%). This is a problem for those living with an ambulatory difficulty, which is experienced by 51% of Ohio adults with a disability.

Ohio's children are more likely than adults to live in poverty; 18% of the population under 18 and 21% of children under 5 are living in households below the federal poverty level – compared to 13% of the overall population.

Homelessness among students remains high. Ohio's public and community schools reported that 26,385 students (1.5% of total enrollment) lacked a fixed, regular, and adequate place to sleep during the 2021–2022 school year.

In 2021, one in three 19-year-olds transitioning out of foster care in Ohio (or 32%) reported experiencing homelessness in the prior two years, which is the highest share among Ohio's neighboring states and a considerably higher likelihood than the national average (21%). At the same time, Ohio's cohort of 17-year-olds exiting foster care is far less likely (16%) to have recently experienced homelessness and less likely than the national cohort at that age (21%).

Ohio's population is relatively old. In 2021, the median age in Ohio was 40 years compared to the national median of 39. Ohio's older adult population also continues to grow, but the amount of growth is slowing down. From 2001 to 2019, Ohioans aged 55 years and over grew steadily from 22% of the population to 31% where the population remains two years later.

Demographers predict the population aged 55 and over will peak between now and 2030. Central Ohio is the only region expected to experience an increase in the older adult population by 2030 (+8.0%) compared to a 2.0% decline statewide.

While the 55-and-over population may be peaking this decade as baby boomers continue to age, older population cohorts are expected to peak in decades to come. By 2050, the number of Ohioans aged 85 years and over will be nearly double in size to what it is now, which poses serious challenges to housing and caring for the elderly.

Although the older adult population may no longer be growing, the number of older Ohioans who live alone is increasing. One of every eight Ohio households – or more than 613,000 – houses a single adult aged 65 or over. Aging householders living alone face unique challenges when it comes to maintaining the cost and upkeep of homes, especially among those who wish to age in place.

One in eight mortgage holders aged 55 and over (13%) is severely housing cost-burdened. Nineteen percent of mortgage holders aged 65 and over and 25% of those aged 75 and over are severely mortgage burdened.

More than 400,000 Ohioans of Color are housing insecure, meaning they live in a household spending at least 50% of its income on housing. Black Ohioans are the most likely racial group to be housing insecure (256,996 people or 19% of the state's Black population). This includes 218,460 living in severely rent-burdened housing (27% of the Black population living in rental housing in Ohio).

The gap in homeownership between white and Black Ohioans has been widening steadily for over a decade to 37 percentage points by 2021 – eight points larger than the national gap (29). Ohio also had the lowest Black homeownership rate compared to neighboring states (36%).

Black mortgage holders are almost twice as likely to be severely mortgage burdened as their white counterparts (14% compared to 8%). This gap is the widest in Northeast Ohio where 17% of Black homeowners with mortgages spend more than half their incomes on housing compared to 8% of white mortgage holders in the region.

Both Black and white potential homebuyers in Ohio are less likely to be denied on a mortgage loan application than they were a decade ago. While the denial rate gap between them has also narrowed, Black Ohioans are still more likely to be denied (26% compared to 15%).

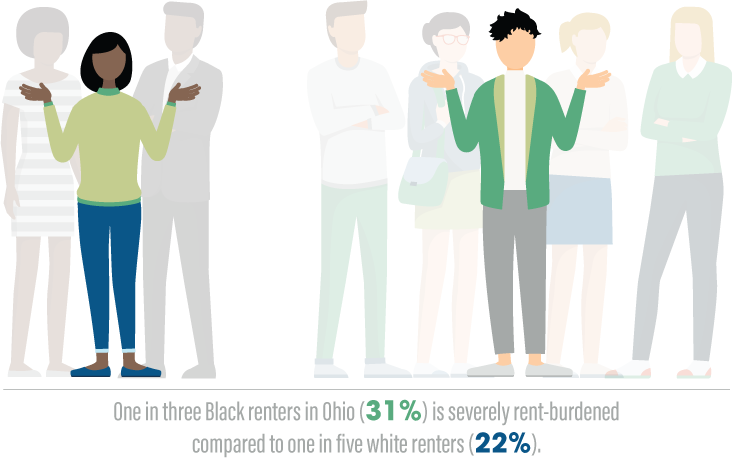

One in three Black renters in Ohio (31%) was severely rent-burdened in 2021 compared to one in five white renters (22%). This gap is widest in Northwest Ohio (11 percentage points) where white renters are the least likely to spend more than half their income on housing (19%) compared to their Black counterparts (30%).

Children born to Black mothers are nearly three times more likely to die before their first birthday than those born to white mothers – 14 deaths per 1,000 live births compared to five. The infant mortality gap between Black and white mothers is the widest in Southeast Ohio where the Black infant mortality rate is the highest in the state – 23 deaths per 1,000 live births. Having safe, quality, and consistent housing improves the chances of survival.

For a more in depth look at the data please visit the Ohio Housing Needs Assessment website.